Online Savings Accounts: rates up to 4.33% AER

✓ Access FSCS-protected savings accounts

✓ Manage all your savings with a single log-in

✓ Discover the ideal product for you from over 40 banks and building societies

Understanding online savings accounts

What is an online savings account?

How do online savings accounts work?

How do online savings accounts differ from traditional savings accounts?

The main difference between online savings accounts and traditional savings accounts is, of course, that you can manage your account online. You can access your account any time you wish, providing convenience if you are unable to visit a branch.

Online savings accounts in the UK often feature more competitive interest rates than traditional accounts. It’s always best to shop around and compare different savings accounts.

Choose the right savings product for your money

Product | Ideal for... | Return | Access to money | Flexibility | Risk |

|---|---|---|---|---|---|

Fixed Rate Bonds | Savers who don’t need access to their money in the short term and want higher returns. | Fixed and competitive return. You know it in advance. | Not accessible until maturity. | Low. You cannot make regular contributions or withdraw funds before the end of the term. | Low. Deposits up to £85,000 per person, per authorised bank or building society are protected by the Financial Services Compensation Scheme (FSCS) in the UK. |

Easy Access | Savers who want liquidity and to earn interest without complications. | Variable return. Competitive interest rates in some cases. | Immediate, if the account offers instant access. | High. You can deposit and withdraw money whenever you like. | Low. Deposits up to £85,000 per person, per authorised bank or building society are protected by the Financial Services Compensation Scheme (FSCS) in the UK. |

Notice Accounts | Savers who want better interest rates than a savings account and can plan withdrawals in advance. | Usually better than standard savings accounts, but lower than fixed-term deposits. May vary with notice period. | Requires advance notice (e.g., 30, 60, or 90 days) before making a withdrawal. | Moderate. Deposits are allowed, but access is subject to the notice period. | Low. Deposits up to £85,000 per person, per authorised bank or building society are protected by the Financial Services Compensation Scheme (FSCS) in the UK. |

View and compare zero-fee savings accounts

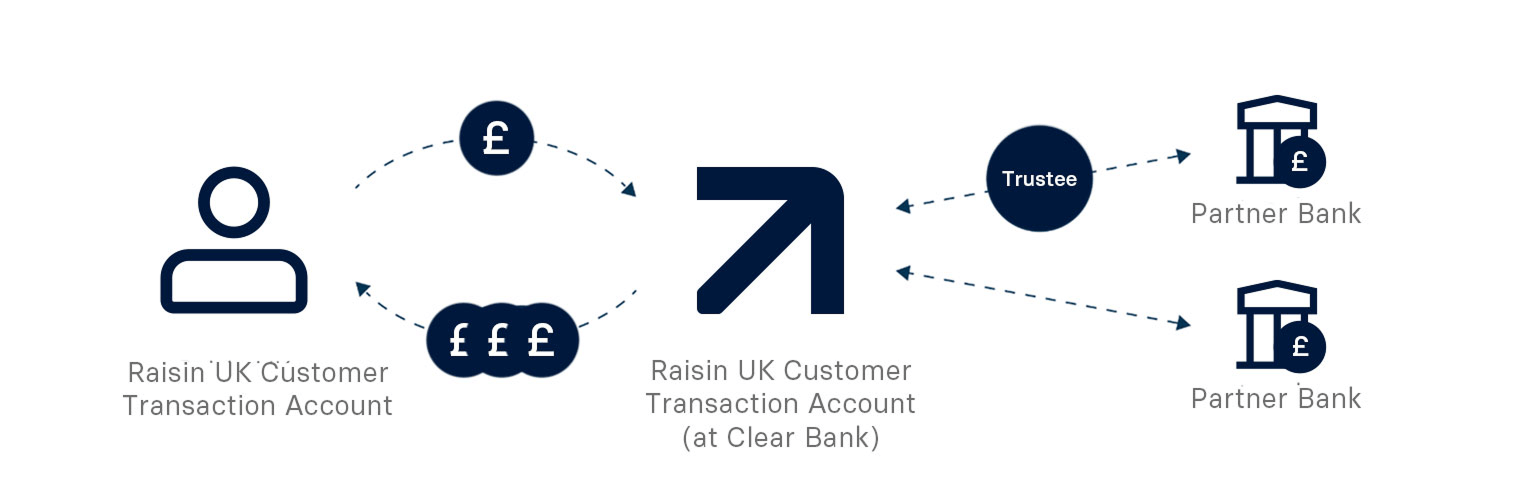

Your money journey

This diagram shows the journey of your money from your bank or building society account to a savings account:

Your money’s journey begins when you transfer funds from your Nominated Account to your Raisin UK Transaction Account, held at Clearbank.

When you place a deposit with one of our partner banks or building societies, the funds are transferred to a bare trustee (Raisin Platforms Limited) or may be transferred directly to your chosen partner bank.

When you choose a product with a partner bank that uses a bare trustee, Raisin Platforms Limited will place the money you wish to invest into your chosen partner bank's savings account and will return your money, along with any interest or profit, to you on maturity. Raisin Platforms Limited has no claim to your funds and administers them on your behalf while providing this service.

To learn more about this process, and the role of trustees, please read our FAQs.

Why should you save with Raisin UK?

Easy money management

Our simple online platform and app allow you to manage your money easily at any time. With all your accounts under one roof, there’s no need to juggle multiple logins, either.

Access to more banks

Why limit yourself to the high street? With more banks at your fingertips from across the UK and Europe, we give you more choice to find the right savings account for you.

Extra savings boosts

From our refer a friend bonus to exclusive savings accounts offers, it’s easy to make your money work harder. We’ll always make sure you’re the first to hear about new top rates, too.